We developed a unique framework that uses multiple years of claims and demographic data to model yearly out-of-pocket cost ranges. Modest savings and regular investing go a long way.

Card swipes are low for 95% of consumers, yet 95% of HSA holders don't invest their HSA dollars.

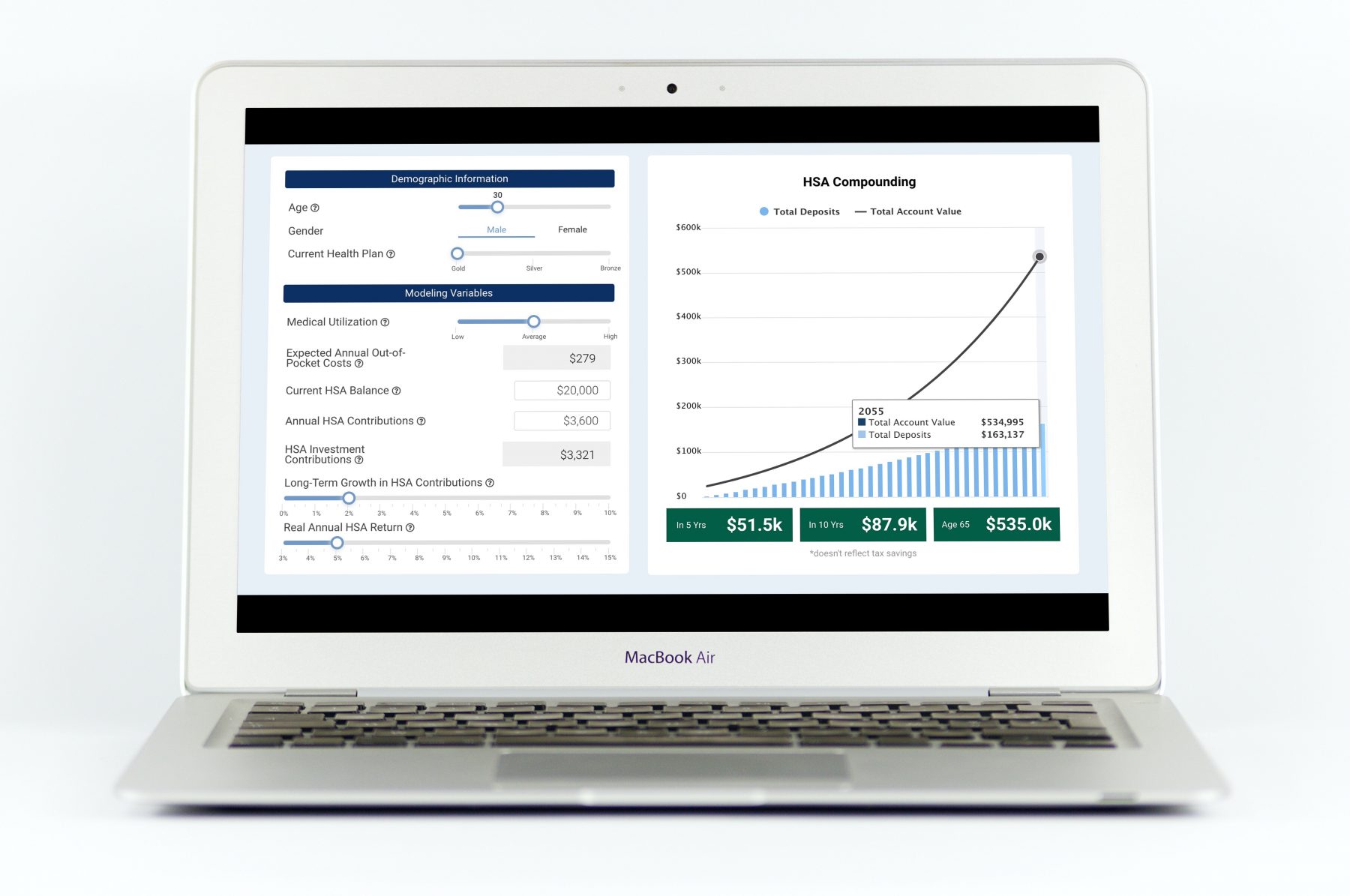

Case Study: Zach Friedman

Goal: Invest my HSA balance for retirement medical expenses and understand my likely current healthcare coverage exposure

- Zach, age 40 is enrolled in a typical healthcare plan ($1,500 deductible).

- His likely annual out-of-pocket costs are $200 to $800, approximately $400 on average based on his age, gender, and plan selection.

- Current HSA balance of $20,000 is idle in cash, earning a negative return after inflation.

- With $200/month in HSA contributions, and a 5% real return on his invested balance, he could have $192,000 dollars by the time he is eligible for Medicare. More than enough to offset premiums and copays1https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs.