They say a great way to lose money is to open a restaurant. Costs, pricing pressures, and low barriers to entry tend to eat into your capital. Dad pun intended. Food, rent and labor inflation are stubborn and every extra dollar counts. All costs matter. Some restaurants make it work and build lasting brands with solid returns on capital, but those are outliers.

Healthcare costs are typically a top 3-4 expense but for some industries, they may matter more than others. Costs understandably vary by industry, geography, tenure, margins (budgets for public sector), or profits. Higher medical costs as a percentage of earnings, sales, or a company’s market value give an overweighted impact to savings. Google, a hyper-productive and cash-rich company, cares more about access and elimination of friction to employees–costs matter less. That’s not the case for a low margin firm trying to find a more stable long-term footing.

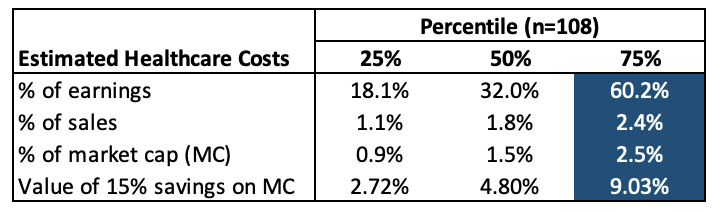

An analysis of 108 micro-cap stocks expands on my previous post, which included just 5 firms. A little background: all 108 firms are US-based, have positive earnings per share, and current market capitalizations of $50 to $300 million. The median employee count is approximately 500. Adjustments and estimates of each employer’s portion of premiums are made for industries, premiums, and take-up rates using Kaiser employer benefits survey data and matched with the firms from the stock screen.

The below table provides a summary. For the 50th percentile firm, a communications equipment company with 500 employees, healthcare costs are 32% of earnings. If cost savings are predictable and sustainable, for each 1% change in healthcare costs, the middle 50% (or interquartile range) of firms have a potential market cap impact of 18 to 60 basis points (1% equals 100 basis points). A 15% reduction in healthcare costs for a top quartile healthcare cost firm could mean a 9% change in market value, assuming current company earnings multiples. For the top 10%, it could mean 20%+. When an earnings beat of a few pennies can move a stock, this commands some attention.

This sounds easy in theory but many companies are jaded by stale promises. Medical trend in the US is 2-3x inflation. Cigna, perhaps the most public on this, has a goal of below-CPI trend, which if reached, amounts to roughly 3% savings–in stock market value that would likely result in a median improvement of 1%.

This caution applies to brokers and consultants. In 2013 one large risk/brokerage firm came out with a corporate healthcare exchange model with the hope of CPI trend for its clients. The model targeted large companies and through multiple insurance companies and a broad menu of plans; each employee has 12-20 choices of plans. In year one, with limited enrollments, they trumpeted 1.8% trend, CPI or less. Their 1.8% vs. 5%+ market trend was supposed to be a big difference. The CEO was brimming with pride. Analysts’ questions poured in. When the staying power of those savings faltered, management changed the subject, and as the head of Investor Relations told me in an email exchange: “There is much more focus on the integration at this time.” The curve of what people brag about over time is telling.

New solutions, contracting, moves to self-insurance, elimination of waste (e.g. bad wellness programs), the right transparent broker relationship, with better incentives, can create 10-15%+ savings. This also has implications on productivity, worker finances, employees’ health, and firms’ market values. When a recession comes this will matter more, as budgets get more scrutiny, and inefficiencies get a closer look. Many firms, including restaurants, could benefit from a new lens, and a new broker-detective who knows where to look and how to align interests.

View-only data, along with some of the number-crunching can be found here.

For further questions or a deeper dive into specific companies and industries, contact [email protected] or Joe at 801-529-7695. The image at the top shows the organization of the New York Stock Exchange in 1792, the famed, Buttonwood agreement.