How much do healthcare costs matter to companies’ earnings? Relative to earnings they’re larger than many think.

24%.

That’s the median estimated healthcare costs as a percentage of earnings for the S&P 1000 (the lesser-known index sibling of the S&P 500).

I ran an analysis of data from S&P 1000 firms and filtered for those with at last 50 employees and positive earnings. I layered on unique data that includes the average healthcare costs per employee by industry*. This group of 800+ firms includes a median 3,200 employees, market caps of $2.2B, and earnings of $100M.

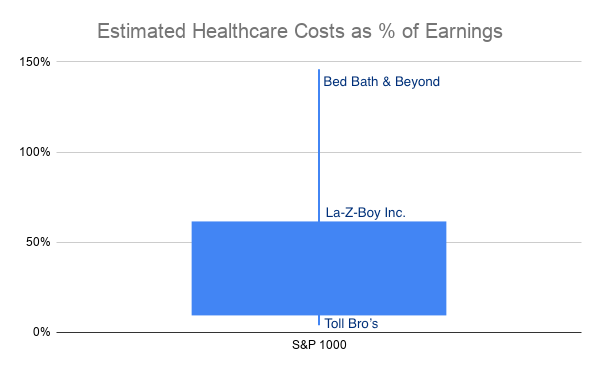

The median is fine but it hides a lot of variation. The earnings impact of the top quartile is 6x more sensitive to healthcare cost inflation than the bottom quartile. The below chart shows the range of variability by percentiles (10,25,75,90th). Some firms generate huge sales with few employees, while others are in low margin businesses. What kind of company is near the top of the most exposed? It’s a diverse bunch. One is Bed Bath & Beyond, the struggling retailer, where healthcare costs are almost 140% of earnings.

Wingstop (a restaurant especially subject to chicken wing, healthcare, and wage inflation) is in the middle of the pack at 24% of earnings. Suppose you save 10% on healthcare costs or a 2.4% positive earnings surprise. Investment is ruled by expectations, and it could be enough to create alpha, or outsized investment returns.

In investment classic Expectations Investing: Reading Stock Prices for Better Returns authors Rappaport and Mauboussin write: “The only investors who earn superior returns are those who correctly anticipate changes in a company’s competitive position (and the resulting cash flows) that the current stock price does not reflect.”

When will it matter to companies as much as it does to healthcare consultants, vendors and brokers? Likely never. Scott Adams, in his fine book Loserthink, reminds us that it is our nature is to assume whatever we think about the most is the most important.

A noble goal is to focus on the facts and work with firms that can consistently deliver savings. Next, hire an advisor whose interests are aligned (incentives for beating trend vs. adding new programs where they make higher commissions even if costs rise). The early innings stage doesn’t describe where companies are in this; we’re seeing the first batters. Do that and investors’ ears will perk up, executives’ bonuses will grow, and employees may even be happier and more productive.

*calculation details: (number of employees)*(% of employees eligible for benefits)*( average industry take-up rate)*(average employer contribution %)*2

Photo by Alec Favale on Unsplash