Index investing is one of the greatest growth stories in finance. Indexing is a form of passive investing, a simple strategy–basically long-term autopilot. Why try to beat the S&P 500 when you can match it? Even Warren Buffett recommends it for others.

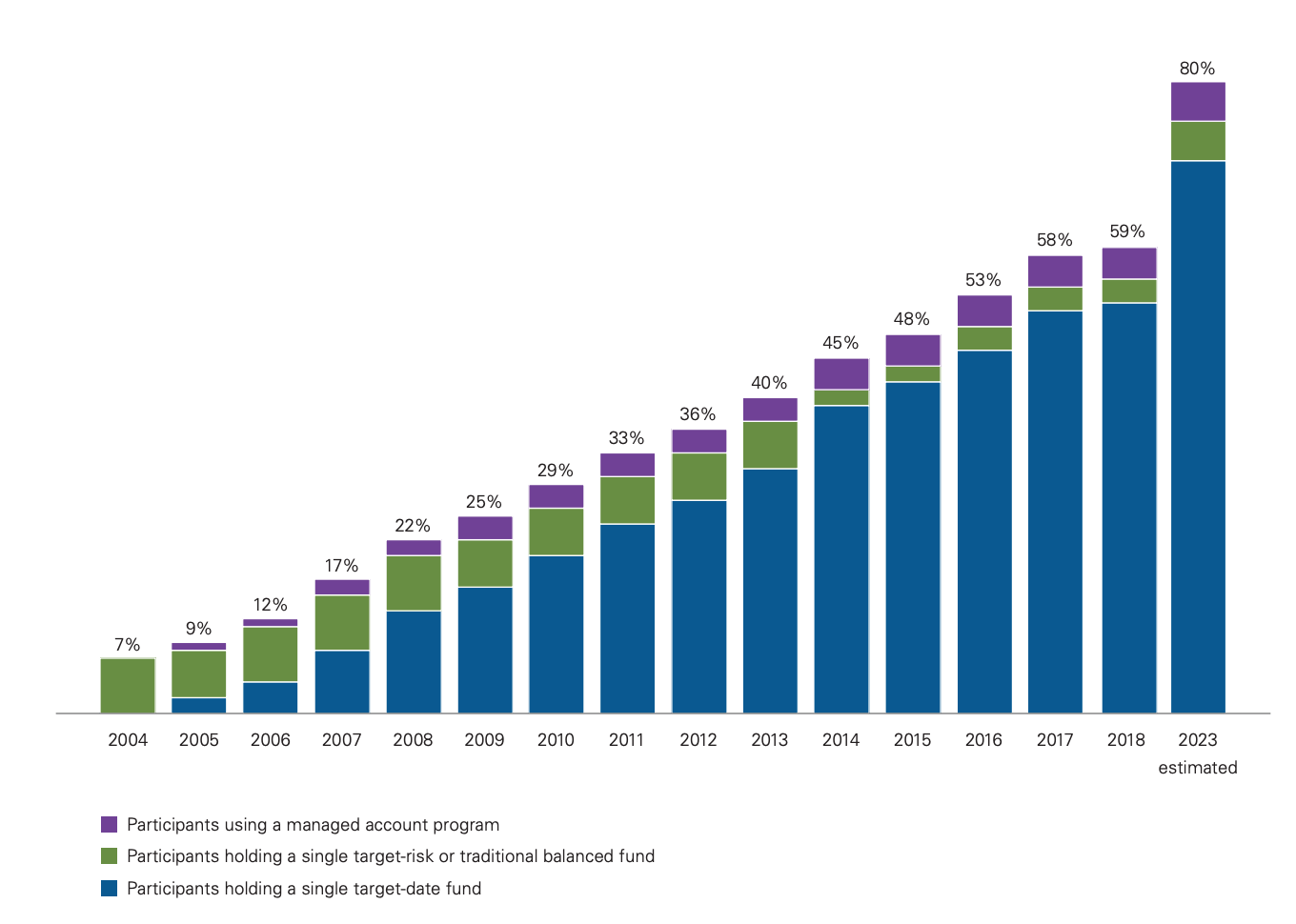

Today, passive strategies control trillions of dollars. A segment of passive, target-date funds (TDFs), a grandchild of John Bogle’s indexing boom, are ballooning, and now stand at over $1.4T1 in assets, now taking in 1 of 2 retirement dollars. The idea is this: an investor’s risk appetite changes over time and so portfolios are automatically rebalanced over time. A 20-year-old should take more risk than a 65-year-old. A Millenial may have 80-90% of a fund in equities and the rest in bonds, a baby boomer closer to a 50/50 split. Software is eating the world but single target-date funds are having their fill too. Witness the takeover in blue in the chart below2.

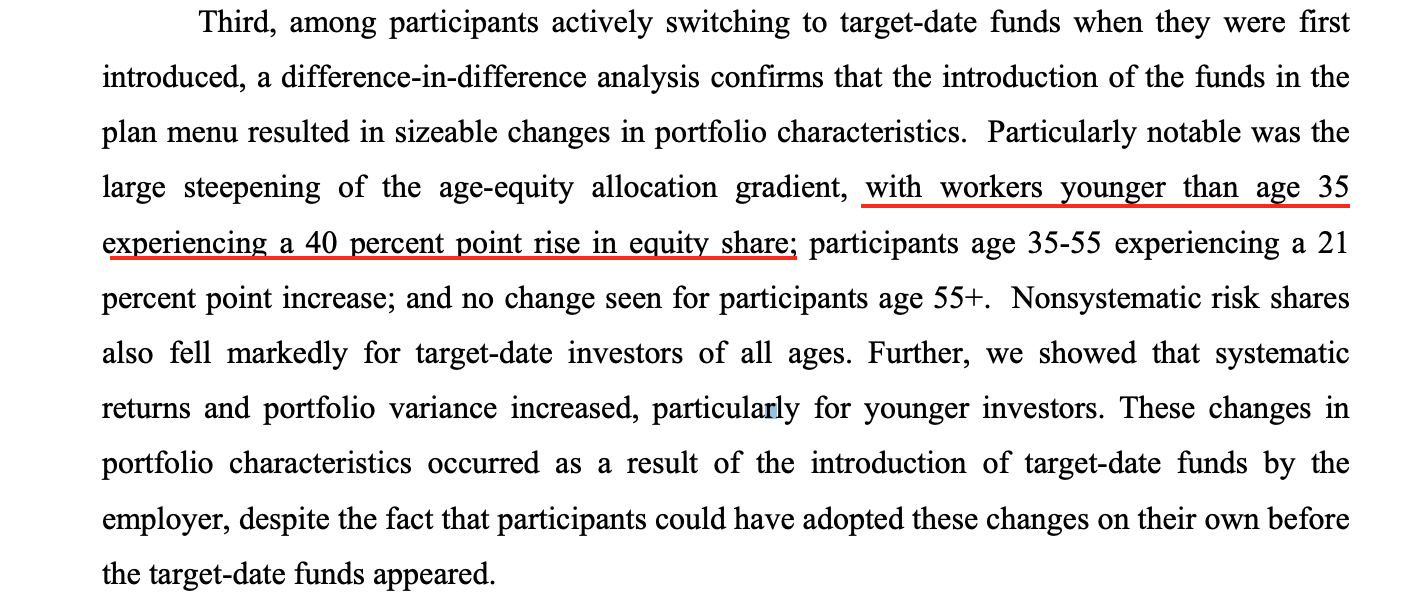

Before target-date-funds, many retirement savers were too risk-averse. One of the greatest contributions of TDFs has been the increase in equity allocation3, for younger workers in particular: an extra 40% allocation towards equities for those under 35 (see below for the 2012 NBER paper by Mitchell and Utkus4). That’s a good bet to outperform bonds for those with a 30+ year runway to retirement. Even slight annual outperformance compounds over time: In 30 years you’d have 32% more money if you earned 8% instead of 7%.

Health Savings Accounts (HSA) are a growing but an underappreciated area of retirement savings; they have lower contribution limits but greater tax advantages. There are now 28 million accounts according to Devenir but only 4-5% of those invest their balances. The others spend their HSA dollars for Junior’s broken arm, a Z-Pak, or a minor surgery. Otherwise, funds are left parked in cash where returns are measured in basis points, fractions of 1%.

Health and wealth are connected. Over-insurance can cost tens of thousands of dollars over time, and investing the difference in premiums is a good start, healthcare 1.0. As HSA investment accounts and balances5 grow, those millions of accounts will start looking for investment vehicles to prepare for 20+ yrs of Medicare out-of-pocket costs6. The human depreciation curve (read: medical utilization curve) is steeper after 60. In working years, most have episodic interactions with the health system, so direct costs for care are often low. Having better investment choices now may help with future costs in retirement. The adequacy of the asset mix may change over time based on healthcare inflation and likely medical expenditures in retirement, perhaps warranting a separate investment allocation strategy. HSAs 3.0. Simple products that help expand that Venn diagram will do well.

Disclosures: my personal healthcare coverage is a $5,000 deductible cost-sharing plan (non-ACA compliant). Healthcare investments: long CI, HQY; short (via long puts): TDOC. I have a Lively HSA and have invested most of the balance in 5 stocks7 via a self-directed TD Ameritrade account.

Photo by Aw Creative on Unsplash

- https://www.investmentnews.com/target-date-sales-returns-up-2019-187835

- Vanguard’s 2019 report: How America Saves

- interestingly, total contributions are flat at 10% of earnings over the last 10 years

- https://www.nber.org/papers/w17911.pdf

- now at $16B

- OOP costs average $5-6k/year per Milliman

- that’s how I roll