Whether Einstein said it or not, compound interest is amazing: “…the eighth wonder of the world. He who understands it earns it, he who doesn’t, pays it.” Negative compounding is powerful too, and we pay it in the form of healthcare inflation.

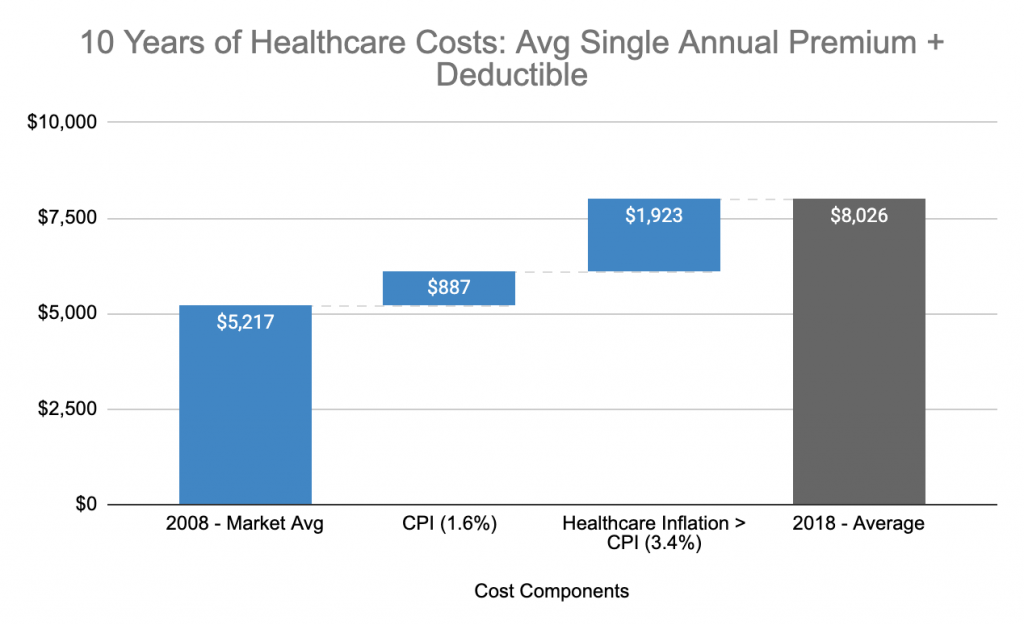

Over the last 10 years, annual healthcare inflation for workers has averaged 5%1, or more than double CPI. 1/3 of that 5% is general inflation, the rest: admin, regulations, wages, new drugs, profits (some excess), waste, etc. In a decade the beyond-CPI number has grown approximately $2,000 for a single employee–see $1,923 in the chart below2 and 3x more for family coverage.

A common crime with charts is to favor shock factor: deductibles are up 212% while wages are up 26% (one of the worst is quoting Dow points–something not relevant since my grandpa traded stocks in the 1940s–percentage movements with stocks is what matters). While true, the bigger story is the dollar impact of those increases.

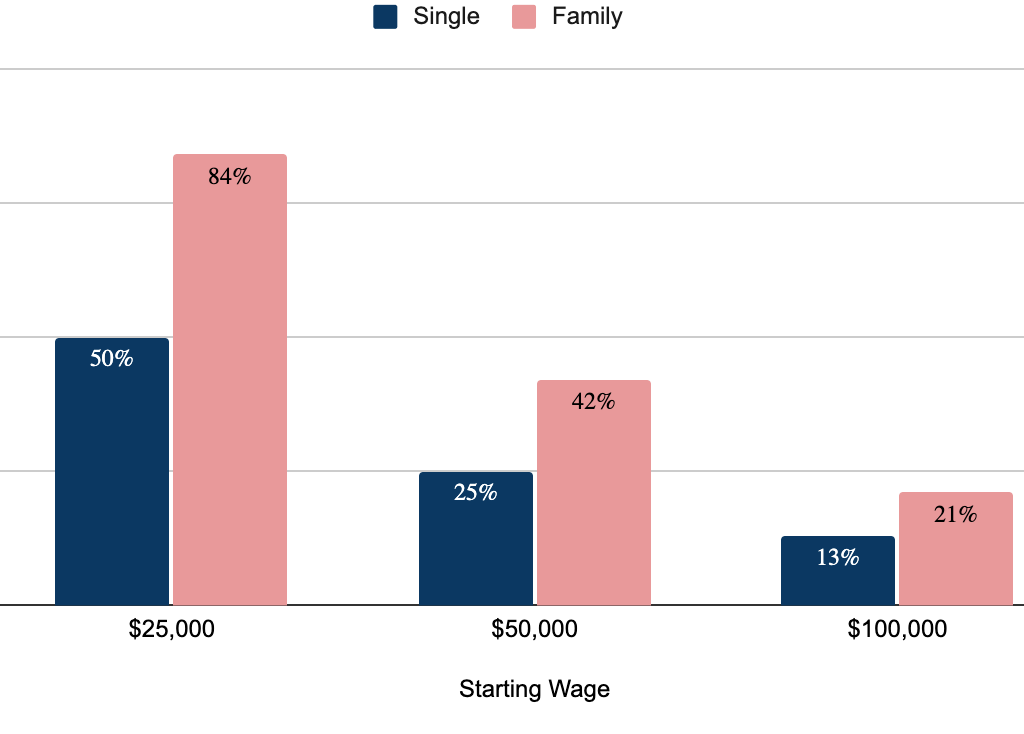

The pain of rising healthcare costs is not distributed evenly. The $2k is added to today’s rising deductibles and premiums and includes additional items such as essential benefits under the ACA (hint: free isn’t free). That $2k is equal to one-quarter of the wage gains3over the last 10 years for a single worker starting out making $50,000 in 2008–42% for family coverage; and a much higher rate for lower-wage workers (see below).

As consumers, we should spend 2x more thinking about healthcare coverage purchasing decisions as we do about a new TV. Consider a direct primary care doctor, a cash membership model like Costco for primary care. If you can join a better risk pool, consider it (an example is choosing a higher deductible plan) and invest the difference in premiums. Know what your benefits are worth–there is a bounty for knowing and negotiating this, thousands of dollars potentially. This video explains it. Every $50 payroll contribution counts, and if invested for the long haul, earns interest that compounds over time.

—

Disclosures: my personal healthcare coverage is a $5,000 deductible cost-sharing plan (non-ACA compliant). Healthcare investments: long CI, HQY, DRIO; short (via long puts): LVGO. My HSA account is with Lively.